A private manufacturer earning $5 million in EBITDA and a publicly traded manufacturer earning the same $5 million are, on paper, the same business. Same product, same margins, same customers. Yet the public company might carry an enterprise value of $60 million and the private one $35 million. Same earnings. A $25 million difference. Nothing about the operating business explains it.

Most owners assume the gap is about size, or growth, or some intangible quality the public company possesses. It isn’t. The gap is structural. It comes from how each type of business is valued, by whom, and under what constraints. Understanding that machinery is the difference between accepting the discount as a fact of life and doing something about it before you sell.

Two Different Pricing Mechanisms

A public company is priced by a continuous auction. Thousands of participants set the price every second the market is open, and that price reflects a vast pool of capital competing for a liquid, tradeable share. If you don’t like the price today, you wait until tomorrow. Liquidity is near-total: you can exit your position in seconds at a known, observable number.

A private company is priced by negotiation. There is no ticker, no continuous auction, no observable price. Value is discovered through a process: a banker, a buyer universe, a data room, a set of bids. The number that emerges reflects who happened to be at the table, how much competitive tension the process generated, and how motivated each side was. The pool of capable buyers is measured in dozens, not millions.

These are not two versions of the same valuation. They are two different mechanisms producing two different numbers for the same stream of cash flow. Once you see valuation as a function of the mechanism rather than the asset, the public-private gap stops being mysterious.

The Discounts That Drive the Gap

this too:

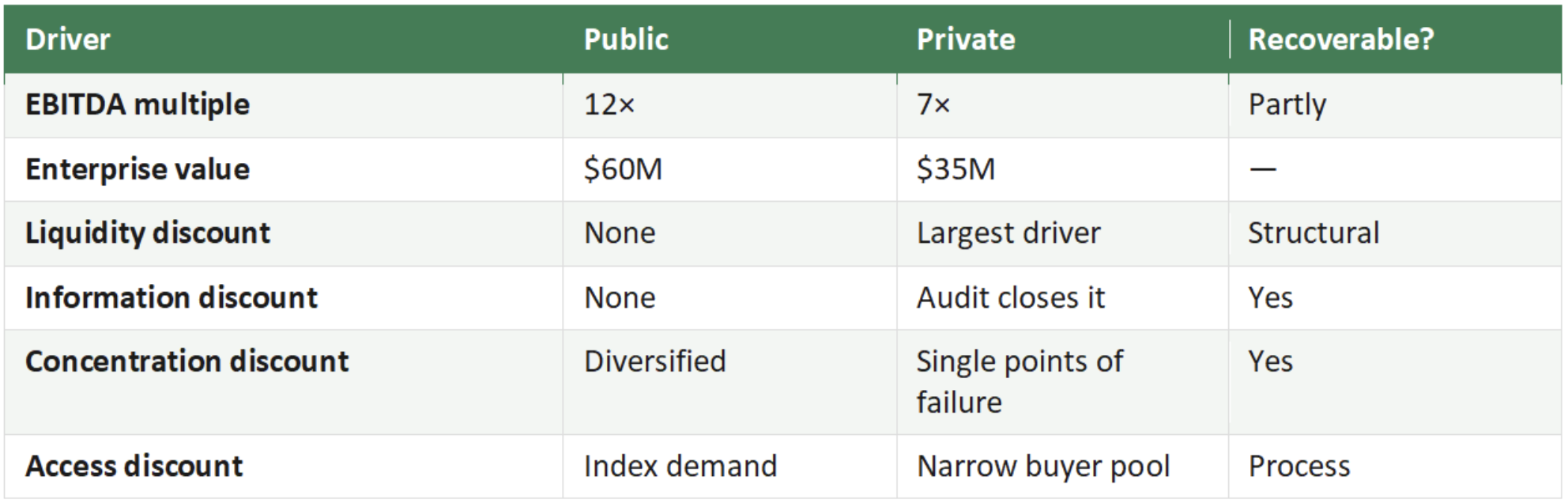

The gap resolves into a handful of specific, nameable discounts. Each is real, each is quantifiable, and — importantly — each is partly within an owner’s control.

The liquidity discount: This is the largest single driver. A public shareholder can sell instantly; a private owner cannot. Capital demands compensation for being locked up, and that compensation shows up as a lower multiple. Empirical studies of the marketability discount have ranged widely, but the working assumption in private markets has long sat somewhere in the 20% to 35% range for a control stake in a healthy private company. The less liquid and the harder to exit, the steeper the discount.

The information discount: Public companies file audited statements quarterly, reconcile to GAAP or IFRS, and submit to analyst scrutiny. A buyer can underwrite a public company with high confidence in the numbers. Private companies often run on owner-adjusted EBITDA, commingled personal and corporate expenses, and financials that have never been audited. Every gap in the information forces the buyer to underwrite risk — and risk is priced as a lower multiple or a larger holdback. Clean, audited, well-documented financials don’t just speed a deal; they directly compress this discount.

The concentration discount: Private companies tend to be concentrated in ways public companies have usually grown out of: one customer at 40% of revenue, one founder who holds every key relationship, one supplier with no backup. Each concentration is a single point of failure, and buyers pay less for fragility. A public company of the same size has typically diversified these risks away, which is part of why it earns a higher multiple.

The access discount: Public equities draw on a global pool of passive and institutional capital. Index funds buy a public company simply because it exists in the index. No such automatic demand exists for a private business. The buyer pool is narrow, often regional, and frequently dependent on acquisition financing — which means the price a private company clears at is hostage to credit conditions in a way a public valuation is not.

A Worked Comparison

Make it concrete. Take two identical industrial services businesses, each generating $5 million in EBITDA.

The public comparable trades at 12× EBITDA, an enterprise value of $60 million. That multiple reflects full liquidity, audited reporting, a diversified customer base, and access to deep public capital markets.

The private business, sold through a traditional M&A process, attracts a 7× multiple, an enterprise value of $35 million. The 5× spread is the stack of discounts above, layered on top of one another: liquidity, information, concentration, and access, compounding into a $25 million difference for the same $5 million of earnings.

Here is the part most owners never internalize: the spread is not fixed. Of those five turns of multiple, perhaps one and a half are genuinely structural, the irreducible cost of being private and illiquid. The rest is addressable. An owner who audits the financials, diversifies the top customer, builds a management team that survives the founder’s departure, and runs a competitive process rather than a bilateral negotiation can recover a meaningful portion of the discount. Moving from 7× to 9× on $5 million of EBITDA is $10 million in additional proceeds, earned not by improving the business, but by changing how it is presented and sold.

The Multiple Hiding Inside the Multiple

There is a further layer that the public-private framing tends to obscure, and it is the one we spend most of our time on. Even within a single private company, not all earnings deserve the same multiple.

If the business owns the real estate it operates from, a portion of its enterprise value is not operating value at all. It is real estate value trapped inside an operating multiple. The market prices the whole entity at, say, 7× EBITDA. But the real estate underneath it, if sold to a net-lease investor, might clear at a 7% cap rate, the equivalent of roughly 14× the implied rent. That is a public-style multiple sitting inside a private company, valued as if it were operating earnings.

“The wrong pricing mechanism is being applied to a stream of cash flow that deserves a better one. The cure is to separate the asset, and let it find the buyer best positioned to pay for it.”

same here: This is the same disease as the public-private gap, in miniature. The cure is the same too — a pre-exit sale leaseback sells the property at real estate prices and the operating business at operating prices, capturing a spread that a single-entity sale leaves on the table. For an owner already absorbing a private-company discount on the operating business, recovering the real estate spread is often the single largest lever available.

Where the Logic Breaks

The public-versus-private framework is a lens, not a law. It misleads in several situations, and it’s worth being honest about them.

-

Public isn’t automatically higher. Small-cap public companies - thinly traded, under-covered, orphaned by the indexes - frequently trade at lower multiples than comparable private businesses commanding strategic interest. Being listed is not the same as being liquid.

-

Strategic premiums override the discount. When a private company holds something a specific acquirer needs - a technology, a license, a foothold in a constrained market - the strategic premium can erase the private discount entirely. Scarcity beats liquidity.

-

Control cuts both ways. Public valuations reflect minority, non-control trading prices. A private sale is almost always a control transaction, and control is worth a premium of its own. Part of the apparent discount is offset by the control premium embedded in the private deal.

-

The discounts aren’t additive in a straight line. Fixing one weakness sometimes resolves another; clean financials can reduce perceived concentration risk because the buyer can finally see the customer data clearly. The stack compounds and uncompounds in ways that require judgment, not a spreadsheet formula.

The Decision That’s Actually Yours

The instinct, when an owner first sees the public-private gap, is to treat it as an injustice, proof that private businesses are structurally underpriced and there’s nothing to be done. That’s the wrong conclusion. The gap is real, but it is not monolithic. Part of it is the fixed cost of being private. The rest is a to-do list.

Audited financials. Customer diversification. A management team that isn’t you. A competitive process instead of a single conversation. And, where real estate sits on the balance sheet, a deliberate decision about whether to sell the building inside the business or alongside it. Each of these recovers a piece of the discount, and the pieces are large.

You will never trade at a public multiple. You don’t have the liquidity, and you shouldn’t price your business as if you did. But the distance between the discount you’ll inevitably absorb and the discount you’ll actually accept is wider than almost any owner realizes. Closing it is the work. The only way to start is to understand which part of the gap is structural and which part is simply waiting for someone to address it.

Leave a Comment